Inventory Management

Procurement

Method Pay

Analytics & Reporting

Sound inventory management techniques are the foundation for strategic procurement, enabling you to:

Choosing the right inventory management processes that suit your dental practice is not a simple task, and the more your business grows, the more difficult managing your inventory can be.

That's why laying the right foundation with a scalable solution is critical for growth.

This article outlines what inventory management entails, its benefits, and the techniques and best practices that make for good inventory management. We'll also dig into how digitization can enable efficiency and make life easier for employees, so they can get on with taking care of patients.

Inventory management is the tracking and managing of inventory from the purchase of goods through to their sale or usage.

Tracking inventory allows you to identify when it's time to order and how much to order, ensuring you always have enough stock of the right supplies to service your patients.

Learning to manage your inventory is the first step in gaining control of your spending so you can stay within budget, minimize waste and leverage your purchasing volumes to reduce costs and improve profits.

Although your supply inventory is needed to produce revenue, it also ties up cash.

Too much inventory impedes your cash flow and puts you at risk of financial hits from expired, lost, or damaged stock.

This is why inventory turnover (how long your inventory sits before it is used) is a good measurement of your inventory management.

Inventory management is a key component of an organization's financial health, as it ensures you carry the appropriate amount of stock to suit your business needs. Carrying too much stock ties up cash and puts you at risk of loss, damaged or expired inventory. But too little inventory can lead to stockouts, damaging your patient care and revenue.

Proper inventory management can also help save you money. By understanding your usage, you can leverage your purchasing volumes for cost savings and take advantage of economies of scale.

Proper inventory management can save you on soft costs (indirect costs such as labor) and make life easier for your employees. By removing the guesswork from buying supplies, streamlining processes, and organizing supplies, employees can more easily reorder supplies and quickly find what they need when they need it.

Your dental office is a busy place but, by taking some moments to review and establish some essential inventory management processes, you can remove some of the chaos while improving profits.

It's a win-win for employees and your balance sheet, providing you with a systematic, scalable approach to managing inventory that optimizes profits and supports future growth.

For dental practices, the goal of inventory management is to know your stock levels, where that stock is located, and identify when it is time to order more and in what quantities.

At its most basic level, the process works by tracking your current stock levels and then adjusting inventory down, as it is used, and up, upon receipt of deliveries. As no system is perfectly executed, inventory counts will lose accuracy over time.

Therefore, physical inventory counts are performed to audit, validate and adjust inventory levels as needed to increase accuracy. The process begins when you identify the requirement for a specific supply.

The item is then sourced, a vendor selected, and an order placed and tracked. Upon delivery and verification of the received item, quantity, and condition (the product must be in good order and fit for use), the quantity received is then adjusted into inventory.

The inventory management process also involves organizing storage and analyzing future requirements by taking into consideration factors that may impact usages such as growth, scheduled services, or holidays to ensure inventory levels suffice and are used as efficiently as possible.

These nine methods and processes will help you to balance your priorities, keeping your practice safe from disruption while taking into consideration the availability of resources and profits.

Based on the famous Pareto principle, the ABC analysis is a way of identifying and categorizing inventory by popularity, with A being your highest movers and C being the least.

The Pareto principle, also known as the 80/20 rule, was founded on the idea that 80% of outcomes come from 20% of causes.

If the principle holds correct, 20% of your supply stock supports production that represents 80% of your profits.The idea isn't that you completely forget about the other 80%, but rather that you focus the majority of your efforts on ensuring the 20% meets its full potential by:

First in, first out (FIFO) is a systematic process for ensuring your oldest stock is used first. This process is essential for supplies with a short shelf life, ensuring you minimize waste from expired products.

It's rather simple to set up. Think of cans on a grocery store shelf. The key is to line up supplies, one behind the other from oldest to newest.

Cycle counting is an auditing process where you physically verify and adjust stock levels to correspond with reality for increased inventory accuracy.

Rather than performing a full count of all inventory at once, which can be extremely time-consuming, the counting method breaks up the counts into more manageable pieces.

Over the years, giants such as Toyota and Motorola have given birth to methodologies that help guide organizational improvements.

Although initially born out of necessity for manufacturing efficiencies, the Japanese methodologies have proven universally effective in reducing waste of any kind (including time) and increasing efficiencies.

The methodologies have since been adopted for businesses of all types and sizes, including Amazon, which uses six sigma to improve customer satisfaction. One of its core principles is lean inventory management, a staple practice for those looking to control costs and maximize profits.

A central part of lean inventory management, JIT focuses on reducing waste and optimizing cash flow by bringing in materials just in time.

Minimizing the time between delivery and use allows companies to safely maintain the lowest stock possible without risking production rates or service levels.

An important part of inventory management is knowing when to reorder.

Based on a formula, reorder point is the minimum stock level that triggers a reorder, ensuring you carry enough on hand to get you through until your order delivers without risking running out.

Economic order quantity is a pre-calculated order quantity that reduces holding costs while also taking into consideration purchasing price, ensuring you order a quantity that makes the most economic sense for your business.

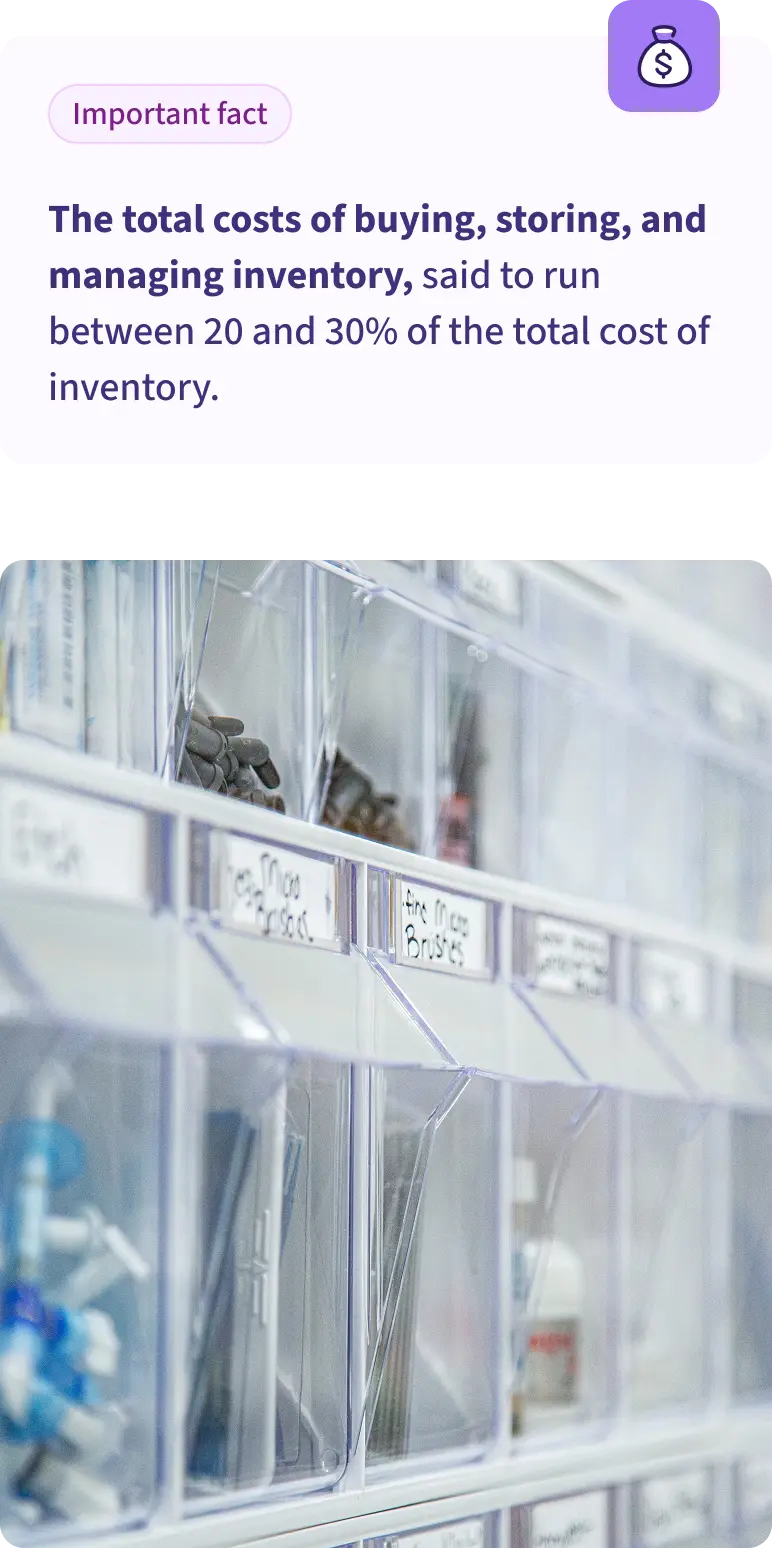

Your order quantity impacts your purchase price, cash flow, and carrying costs (the total costs of buying, storing, and managing inventory, said to run between 20 and 30% of the total cost of inventory).

Therefore, it's important to get it right and not make such an important call on a whim. Your order quantity should be carefully calculated with consideration given to your expected usage, the average lead time for the product (the time between placing an order and when it delivers), shelf life, your practice's financial situation, and any physical holding limitations.

Safety stock is extra stock you carry with the explicit intention to act as a buffer, helping you to mitigate the risks of stockouts in case of any uncertainties such as inventory discrepancies or disruptions in supply.

There are different methods for determining your safety stocks, depending on your priorities and how much risk you're willing to take. Depending on your inventory management system, your safety stock may be calculated into your reorder point.

MRO stands for maintenance, repair, and operating. These items are required to run your practice but do not directly support the production process.

As they aren't required to service your patients, the items typically aren't tracked and follow a different ordering process than your inventory items. They may even be managed by different employees.

MRO items include office or janitorial supplies, technology, or other tools and components required for maintenance, repairs, and operating.

When deciding how to improve your inventory management, you must look at your business priorities and the resources you can allocate. Here's some food for thought.

When it comes to profits, you can either look to increase revenue by buying more practices or adding more chairs, or decrease your overhead costs. When it comes to increasing revenue, tactics that drive revenue growth, such as marketing, are high risk. There's no saying you can get more patients into your door simply because you've poured money into marketing and scaling.

Additionally, only a portion of your revenue makes it to your bottom line, as you must first subtract your overhead. We've estimated that saving one dollar is equivalent to generating $2.94 in production revenue.

While you can always do both, by prioritizing improving your inventory management and establishing a scalable process, you can ensure sustainable profit growth.

You may feel some loyalty to long-standing suppliers, and that's okay.

But even long-standing suppliers should be willing to work hard to maintain your business. Let them know you're paying attention to your costs and are looking to start leveraging your volumes for price reductions.

Data is power, giving you the information you need to reduce your supply costs and better manage your inventory by setting reorder points and order quantities that make the most economic sense for your business.

To take advantage of economies of scale and reduce costs, you'll need to limit the number of SKUs you purchase and gain control of your purchasing habits.

Establishing a formulary that your employees must abide by when purchasing supplies is the first step in that direction.

If you haven't already, create a supply budget and stick to it. Your supply budget should be a part of your overall dental practice budget.

If you don't already have one and aren't sure where to start, we’ve got you covered in How to Create a Dental Practice Budget.

To control spending and help you stay within your budget, implement an order approval process where those in charge of your financial outcomes approve orders before they are place. This is one area where digitization is key.

This leads us to…

Without technology, inventory management can be extremely time-consuming, limiting your ability to buy smarter and significantly reducing your supply costs. Given the impact that improved inventory management can have on your practice and profits, it may be time to digitize your processes. Let us show you the difference digitizing with Method can make.

Effectively managing the long list of SKUs you require to run your dental practice may sound simple, but it is far from an easy task.

Knowing what, when, and how much to order for every item can quickly become complicated.

Yet, dental practices simply can't afford to overbuy and overpay.

The principles of lean inventory help to create efficiencies, helping you do more with less — an imperative during a human resource crunch.

As a result, many growing dental practices graduate to an inventory management platform with capabilities that go far beyond spreadsheets and formulas.

The principles of lean inventory help to create efficiencies, helping you do more with less — an imperative during a human resource crunch.

By lowering the cost of doing business, you increase your profitability.

And by calming the chaos that can come from the management of supplies and creating a standard process, you reduce the pressures on employees and allow them to bring you increased value by doing the things they do best.

By implementing streamlined digital lean inventory management techniques, you free up your cash and your people so they can do more impactful things for your dental practice.

Ready to improve profits and better manage your inventory?

Method gives dental practices and DSOs the necessary inventory management capabilities to succeed. Our full end-to-end inventory management system makes ordering dental supplies straightforward and hassle-free.